A structural capital misallocation across the majority of the United States—and the largest untapped opportunity for durable venture returns.

The Great 38™ is a geographic and economic framework that identifies a persistent, multi-decade misallocation of venture and growth capital across most of the United States.

Despite representing the majority of the nation’s population, labor force, research institutions, industrial capacity, and real-economy output, the states that make up The Great 38™ receive a disproportionately small share of venture capital investment relative to their economic contribution.

This imbalance is not explained by talent quality, entrepreneurial intent, innovation output, or economic fundamentals.

It is explained by capital concentration dynamics.

The Great 38™ framework exists to name, define, and correct this structural inefficiency.

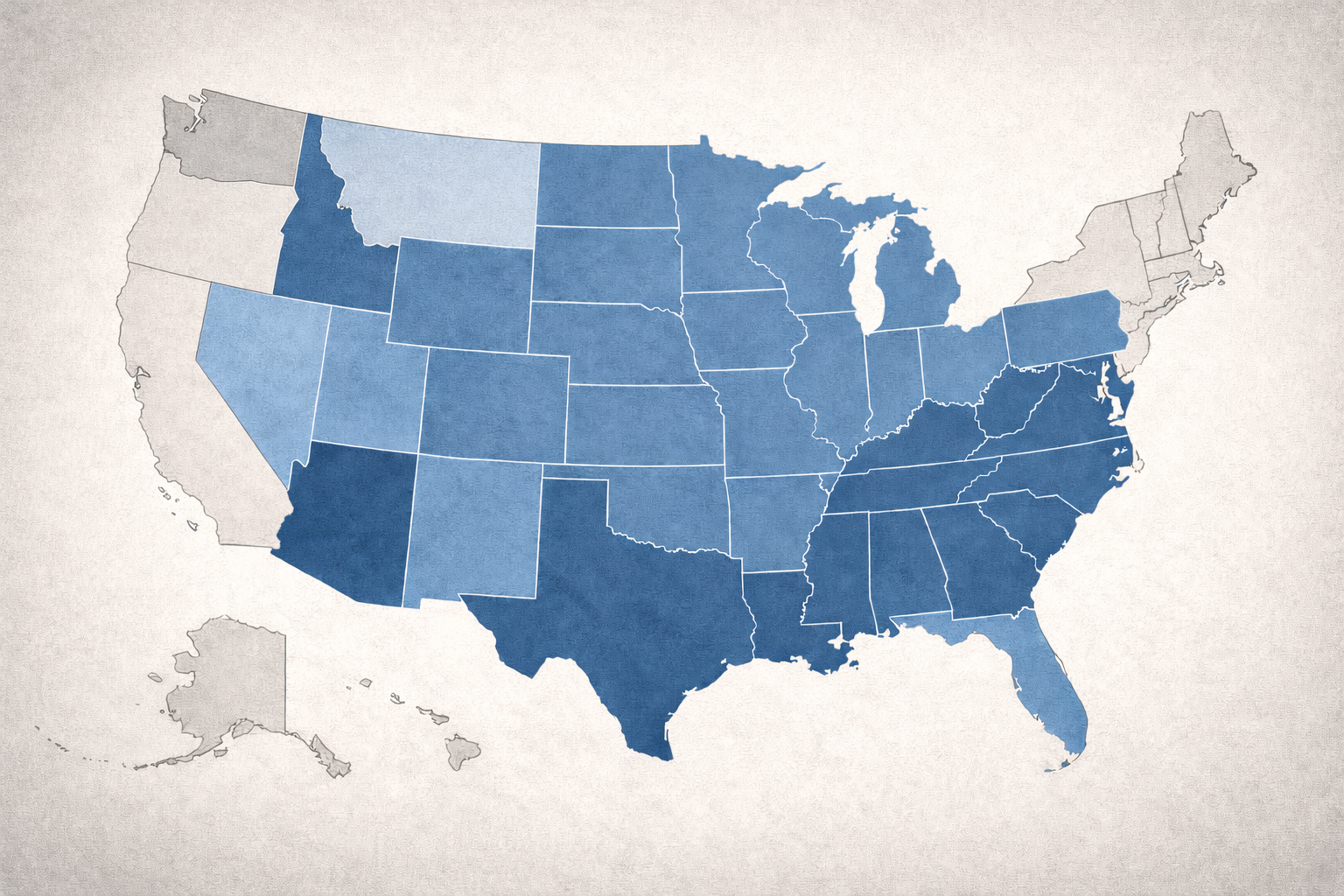

South

AL, AR, DE, DC, FL, GA, KY, LA, MD, MS, NC, OK, SC, TN, VA, WV, PA

Midwest

IL, IN, IA, KS, MI, MN, MO, NE, ND, OH, SD, WI

Mountain West

CO, ID, MT, NV, UT, WY

Southwest

AZ, NM, TX

These 38 states collectively account for:

Yet they receive a minority share of venture capital deployment, particularly at Series A and beyond.

Multiple longitudinal analyses show that U.S. venture capital has become increasingly geographically concentrated, with a small number of coastal metros capturing the majority of late-stage and mega-round funding—even as startup formation and early-stage activity broaden nationally.

By 2024:

This concentration persisted despite evidence that:

Research from universities, venture monitors, and institutional analysts consistently shows that the states within The Great 38™:

Yet founders in these states experience:

This is not a pipeline problem.

It is a throughput problem.

High-potential companies stall or exit early due to capital constraints, not market failure.

Over-concentration amplifies systemic risk by correlating portfolios to the same geographic, labor, and cost structures.

Founders and skilled operators relocate to capital centers, weakening regional ecosystems and reinforcing concentration.

When the majority of the economy compounds slowly while a few regions overheat, aggregate resilience declines.

Institutional research has repeatedly shown that geographic diversification improves portfolio stability and long-term return profiles.

When evaluated through an Enduring Capital framework, The Great 38™ exhibit characteristics that traditional venture models underprice:

These attributes do not maximize velocity.

They maximize survivability and compounding.

The Great 38™ remains undercapitalized because venture capital, as an asset class, has optimized for:

Capital flows where it is already concentrated.

This reflex reinforces itself.

Independent research from universities, venture monitors, and institutional analysts demonstrates that:

The Great 38™ represent a portfolio imbalance, not an ideological argument.

To reprice geographic risk and opportunity as a first-order variable in portfolio construction.

To contextualize capital scarcity as a structural condition, not a signal of founder quality.

To inform LPs seeking durable, diversified exposure beyond overheated markets.

To align capital deployment with where economic output and innovation actually occur.

The Great 38™ names the gap between where capital flows and where value is built.

It is not a call for redistribution.

It is a call for better underwriting.

Capital that seeks endurance rather than velocity must eventually move beyond familiarity and toward fundamentals.

Understanding The Great 38™ is the first step toward reallocating capital for what actually endures.